Tax Deductions for Education Loans Section 80E: For millions of Indian students pursuing their goals, whether it is a master’s degree overseas, an MBA from IIM Ahmedabad, or a B. Tech from IIT Bombay, education loans are a lifeline. With school expenses skyrocketing (₹10 lakh+ for professional courses) and over 100 million retail borrowers in India by 2025 (according to RBI forecasts), loans assist close the gap. Here’s the bright side, though: By providing tax deductions for interest paid, Section 80E of the Income Tax Act of 1961 allows you to recoup your investment. This advantage can alleviate your financial strain, whether you’re a professional in Mumbai managing your EMIs, a parent in Bangalore helping your child with their education, or a student in Delhi repaying a ₹5 lakh loan.

With examples, advice, and actions specifically designed for the Indian audience, we’ll go over what it is, who is eligible, how to claim it, and how much you may save. Now is the ideal moment to learn about this tax exemption because tax season is quickly coming (July 31, 2026, for FY 2025-26) and India’s digital economy is expanding (UPI recorded 14.4 billion transactions in February 2025). Let’s begin using Section 80E to help you save money right now!

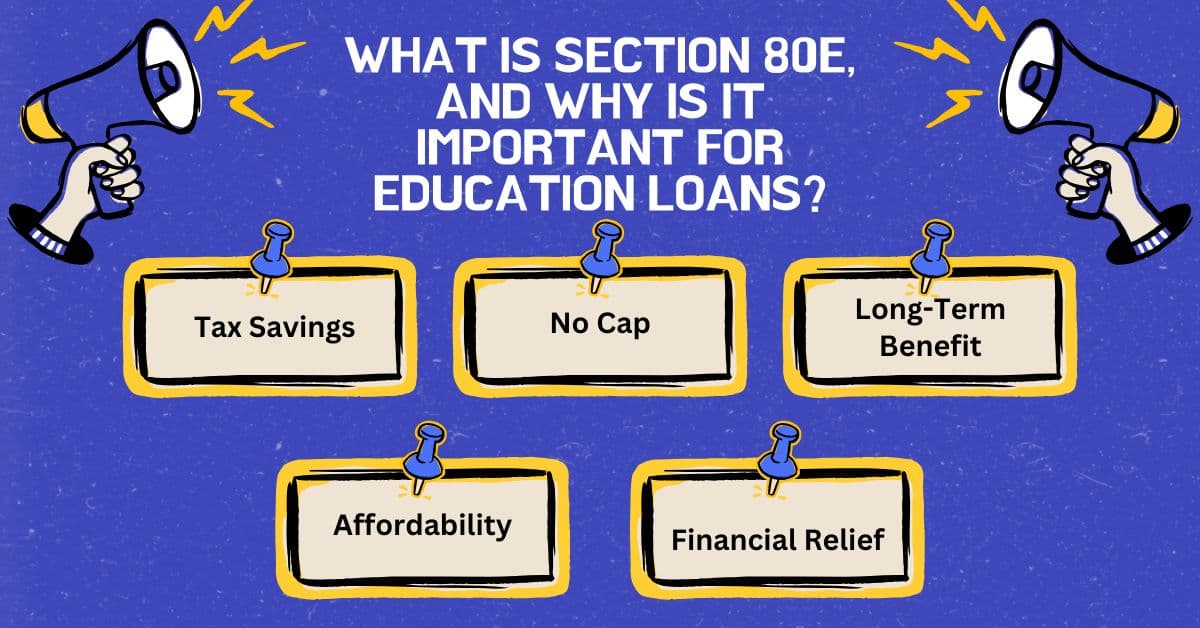

What is Section 80E, and why is it important for education loans?

You can deduct the interest paid on an education loan from your taxable income under Section 80E of the Income Tax Act of India. Section 80E is a potent weapon for borrowers since it is no maximum limit on the interest you may claim, unlike Section 80C, which caps investments like PPF at ₹1.5 lakh. It was introduced to encourage higher education and covers loans for a degree in India or overseas that you, your spouse, or your children take out.

Why it’s important:

- Tax Savings: ₹10,400 (including 4% cess) is saved by claiming ₹50,000 in interest under the 20% slab.

- No Cap: Save ₹31,200 in the 30% slab by claiming ₹1 lakh in interest.

- Long-Term Benefit: Covers the majority of loan terms and is deductible for up to eight years.

- Affordability: Lowers the actual cost of student loans; for example, 9% interest is equivalent to 6% after taxes.

- Financial Relief: Provides funds for other objectives, such as saving.

With interest rates ranging from 8 to 14% and an estimated ₹1.5 lakh crore in student loans by 2025, Section 80E is crucial information for Indian taxpayers. Let’s dissect it.

Understanding Tax Deductions Under Section 80E

What You Are Only Entitled to:

- Only the interest component of your EMI qualifies; principal repayments are not eligible.

- For instance, a ₹5 lakh loan with a 10% interest rate spread over seven years, with ₹10,000 in EMIs, contains ₹4,000 in claimable interest and ₹6,000 in principal.

Who Qualifies:

- Borrower: You, the individual taxpayer, not HUF or businesses, are the borrower who qualifies.

- Purpose: Loans for post-graduation, vocational, and higher education courses are the goal.

- Eligible Loans: Loans from NBFCs (Bajaj Finance), banks (SBI, HDFC), or other authorised financial institutions—not friends or family—are eligible.

- Beneficiary: You, your spouse, your kids, or your legal guardians.

Duration:

- Claim duration is eight years, beginning the year you start making interest payments and continuing for eight years in a row or until the loan is paid off in full, whichever comes first.

- For instance: Repayment begins in April 2025 and can be claimed through March 2033 (FY 2032–2033).

Old Regime Tax Slabs, 2025

- 5%: ₹1,560 on ₹50,000 interest, or ₹2,50,000 to ₹5,00,000.

- Twenty percent: ₹5,00,001–₹10,000,000 (₹10,400 on ₹50,000).

- At least ₹10,000,000 (₹15,600 on ₹50,000) is 30%.

How to Take Advantage of Section 80E Tax Deductions for Education Loans

With advice, examples, and procedures specifically designed for Indian borrowers, this is your comprehensive guide to collecting Section 80E benefits.

Step 1: Verify Your Qualifications

- How to Proceed: Verify the borrower (you, your spouse, or your kid), the lender (an authorised institution), and the loan purpose (further education).

- Why It Is Important: Loans from family members or for K–12 education are not eligible;

- for example, ₹2 lakh from an uncle is not. instance, Priya’s ₹1 lakh friend loan is not eligible, while Anil’s ₹5 lakh SBI loan for his MBA is.

- Take action: By April 15, 2025, confirm loan documentation.

Step 2: Compile the necessary paperwork

What You Require:

- Loan agreement (lender, purpose).

- Interest certificates, which divide EMI into principle and interest, are issued by banks and NBFCs.

- Form 16 (which displays taxable income if you are salaried). Acknowledgement of ITR (if lodged in the preceding year).

Why It Is Important: Smooth claims are ensured by proof—a certificate is required for ₹50,000 interest.

For instance, Sunita’s claim was supported by her ₹40,000 HDFC interest certificate.

Take action by April 20, 2025, to get an interest certificate.

Step 3: Calculate your interest Paid

- How to Proceed: Look at your EMI account; for example, ₹10,000 EMI on ₹5 lakh at 10% is ₹50,000 interest in Year 1.

- The Reason It Works: Only interest is deductible; the entire EMI of ₹1.2 lakh is not deducted from taxable income; only ₹50,000 is.

- In-depth: Interest is larger in the first year (₹50,000) than in the fifth year (₹20,000) (amortisation).

- For instance, Ravi paid ₹60,000 in interest in 2025 and completely claimed it.

- Take action by April 25, 2025, to calculate 2025 interest.

Step 4: Submit a Form Under the Previous Tax System

- How to Proceed: The 2020 regime avoids 80E deductions, therefore choose the previous one.

- Why It Is Important: Old regime interest of ₹50,000 saves ₹10,400 (20% slab); new regime interest saves ₹0.

- Hacks: Compare regimes; if deductions (80C, 80E) are more than exemptions, the old regime wins.

- For instance, the previous system saved ₹15,600 compared to the new one on Priya’s ₹8 lakh income plus ₹50,000 in interest.

- Action: By April 30, 2025, select the previous regime.

Step 5: ITR Claim Deduction

- How to Proceed: Enter interest under “80E” in “Deductions” on your ITR-1 (salaried) or ITR-2 (others) form.

- The Reason It Works: reduces taxable income from ₹6 lakh to ₹5.5 lakh, with interest of ₹50,000.

- Deep Dive: No cap: ₹31,200 saved (30% slab + cess) equals ₹1 lakh interest.

- For instance, Anil’s tax was reduced from ₹62,500 to ₹46,900 (20% slab) due to his ₹60,000 interest.

- By May 05, 2025, practise filling your ITR on ClearTax.

Step 6: Monitor Your Eight-Year Timeframe

- How to Proceed: Take note of your initial repayment year; for example, April 2025 begins FY 2025–2026 and is claimable through FY 2032–2023.

- Why It Is Important: The 8-year restriction is rigorous; if you miss a year, you lose it.

- Hacks: Put the commencement of repayment on your calendar and claim the high interest from the first few years (₹50,000 vs. ₹10,000 thereafter).

- For instance, Sunita began in 2024 and saved a total of ₹80,000 by filing claims through 2032.

- Action: By May 10, 2025, set a reminder for FY 2025–2026.

Step 7: Add to Other Subtractions

- How to Proceed: Combine the 80E with the 80C (₹1.5 lakh—ELSS, PPF), and the 80D (₹25,000—health plan).

- The Reason It Works: ₹62,400 (30% slab) is saved after deducting ₹2 lakh (₹50,000 (80E) + ₹1.5 lakh (80C).

- For instance, Ravi’s ₹1.6 lakh off taxable income is equal to his ₹60,000 interest plus ₹1 lakh PPF.

- Take action: By May 15, 2025, budget ₹50,000 80C.

Step 8: Increase Savings by Prepaying

- How to Proceed: Utilise incentives (₹20,000) to lower principal, which lowers interest and prolongs the advantages of 80E.

- Why It Is Important: Prepaying ₹50,000 on ₹5 lakh (10%, 7 years) saves ₹35,000 in claimable interest.

- Hacks: Make the most of your early years with no prepayment penalties on university loans.

- For instance, Anil paid ₹30,000 in advance, saving ₹3,120 in taxes and ₹10,000 in interest.

- Take action: By December 2025, arrange a ₹10,000 down payment.

Step 9: Make a Family Loan Claim

- How to Proceed: If you are repaying for your spouse or kid, deduct interest (for example, ₹40,000 for your son’s MBBS).

- The Reason It Works Broad eligibility: ₹12,480 saved (30% slab) equals ₹40,000 interest.

- In-depth: You have to be the borrower; parents who are also co-borrowers are eligible.

- For instance: Priya saved ₹15,600 by claiming ₹50,000 for her daughter.

- By May 20, 2025, confirm the borrower’s status.

Step 10: Steer clear of typical blunders

- What to Do: Avoid omitting interest documentation, filing late, or claiming principal.

- Why It Is Important: Notices are triggered by errors—a certificate, not a guess, is required for a ₹50,000 claim.

- Hacks: File by July 31, 2026 (FY 2025–2026); reimbursements are forfeited for late filing.

- For instance, Sunita’s ₹10,000 reimbursement was delayed since her certificate was absent.

- By May 25, 2025, double-check the documents.

Step 11: Make Use of Electronic Resources

- How to Proceed: File using Quicko—auto-calculate 80E—and ClearTax.

- The Reason It Works: saves time and mistakes—in just five minutes, ₹60,000 in interest was input.

- Hacks: AI detects interest paid when bank statements are linked.

- For instance, after 20 days, Anil received a return of ₹15,600 for filing on Quicko.

- Take action by May 30, 2025, to test ClearTax.

Step 12: Make a Post-Loan Wealth Strategy

How to Proceed: After repayment, transfer ₹10,000 in EMI savings to SIPs.

Why It Is Important: Wealth is created using ₹10,000 per month at 12% interest for ten years, or ₹23 lakh.

For instance, in only five years, Priya’s ₹12,000 EMI was converted into a ₹5 lakh SIP corpus.

Take action: by June 05, 2025, by initiating a ₹500 SIP.

How Much Can Section 80E Save You?

Section 80E of the Income Tax Act offers substantial tax savings if you’re paying interest on certain financial instruments, such as an education loan. Your income tax slab determines how much you really save. For example, you may save about ₹2,600 in taxes yearly (including 4% cess) if you pay ₹50,000 in interest each year and are in the 5% tax band. This comes to ₹20,800 over eight years. The same interest payment saves you around ₹10,400 a year under the 20% tax rate, which adds up to ₹83,200 over eight years. Tax savings for those in the 30% tax rate might reach ₹15,600 year, or ₹1,24,800 over eight years .You might save an incredible ₹31,200 year if you’re paying ₹1,00,000 in interest under the 30% slab. This would add up to ₹2,49,600 in total tax savings over eight years. These figures unequivocally demonstrate how carefully using interest deductions may result in significant tax advantages in India, particularly for high-income individuals.

Benefits of Section 80E

- Big Savings: Savings of between ₹50,000 and ₹2.5 lakh over a period of eight years.

- Credit Boost: Tax relief plus timely EMI equals 750+ CIBIL.

- Education Push: Reduces the cost of loans—a ₹10 lakh course feels more manageable.

- Flexibility: No cap—claim interest of at least ₹1 lakh.

- Future-Ready: Goals and SIPs for savings funds.

Examples from Real Life

The MBA Loan of Anil

Anil, a Hyderabad native who is 25 years old and makes ₹8 lakh:

- Loan amount: 5 lakh rupees, 10% interest, 60,000 rupees (Year 1).

- Refund within 30 days; saved ₹18,720 (30% slab).

- He claims that 80E reduced his EMI stress.

Priya, a 40-year-old Mumbai parent with an annual salary of ₹12 lakh, has an MBBS daughter.

- Loan amount: ₹10 lakh, interest of ₹80,000, 9%.

- ₹24,960 (30% slab) — 8 years = ₹1.5 lakh is the amount saved.

- “It’s a family victory,” she says.

Sunita, a 28-year-old Pune native with an annual income of ₹6 lakh, is an overseas master’s student.

- Loan: ₹7 lakh with interest of ₹50,000 and 11%.

- ₹10,400 (20% slab)—₹60,000 over six years was saved.

- “My SIP was funded by tax relief,” she says.

Additional Advice for Borrowers

Applying Early: 15 days for reimbursements if you file by April 2026 (FY 2025-26).

Festive Bonus: Get additional interest by prepaying ₹10,000.

Digital Ease: 5-minute ITR using Quicko and TaxSpanner.

Parent Assistance: Split benefits are claimed by co-borrower parents.

Loan Tenure: Extend to 8 years—80E at most.

Wishfin offers a CIBIL Check for free; 750+ aids in refinancing.

Learn: 80E tips on YouTube (e.g., CAclubindia).

Typical Problems and Their Solutions

- Problem: No certificate of interest.

Solution: Bank request: ₹10,000 loss vs. ₹50 penalty. - Problem: A new regime was chosen.

Solution: Revert to the previous method, which saved ₹15,600 compared to ₹0 for ₹50,000 interest. - Problem: The deadline was missed.

Solution: Submit before July 31, 2026; there will be a ₹5,000 late fee. - Problem: Confusion among the principal is the challenge.

Solution: Check the EMI split—interest only for 80E—as a solution. - Problem: Doubts about foreign loans.

Solution: Verify that approved lenders (like SBI and HDFC) are eligible.

Why India’s Section 80E Is Great

With a market value of ₹1.5 lakh crore (2025), education loans are flourishing in India. Section 80E is ideal:

- Policy Push: Encourages education with an annual payout of ₹50,000 crore.

- Digital Shift: 70 million taxpayers benefit from e-filing and UPI, which simplify claims.

- Economic Need: Relief is required due to rising prices (₹10 lakh courses).

Resources and Tools

- Apps: include Quicko (tax planning), ClearTax (ITR), and TaxSpanner (regime selector).

- Websites: Moneycontrol (advice) and Income Tax India (rules).

- Freebies: include YouTube instructional and EMI calculators from BankBazaar.

- Communities: For tax guidance, see r/IndiaInvestments.

Get Your 80E Deduction Back Today

Use Section 80E to begin saving right away:

- Collect documentation by April 15, 2025.

- Interest must be calculated before April 25, 2025.

- By July 31, 2026 (FY 2025–26), file your ITR.

In addition to helping people advance their professions, education loans also reduce taxes. To distribute the wealth, provide this information to parents or students. Every Indian borrower benefits from Section 80E!

Let AI Boost Your Tax Refund – Here’s How!

How to Use Section 80C for Tax Planning: A Beginner’s Guide!

Capital Gains Tax in India: Everything You Need to Know!